NTJ

National Tax Journal — Working Paper

Moral hazard in §45Z credit verification: an economic framework for independent observation

Aurea L. Rivera, P.E., F.NSPE, PMP, PMI-ACP

Abstract

The §45Z Clean Fuel Production Credit creates a verification architecture in which tax-credit value depends in part on upstream agricultural practices that are difficult for the government to observe directly at the field level. This paper applies the economic theory of moral hazard — beginning with Arrow (1963) and Pauly (1968) and extending through the observability literature of Holmström (1979) and Shavell (1979) — to analyze that structure.

The paper argues that the current framework contains the core conditions under which moral-hazard risk becomes analytically salient: information asymmetry between reporting and relying parties, and partial cost displacement when inaccurate claims increase credit value but the public bears the excess disbursement risk. Rather than estimating realized overstatement, the paper develops a stylized welfare-loss framework to show how weak observability can generate incentives consistent with systematic overstatement.

It then argues that independent physical observation is the economically relevant ex ante remedy because it reduces information asymmetry before claims are filed. The policy implication is not that producers are dishonest, but that a high-value tax-credit system should not rely predominantly on self-reported upstream facts when independent observation is increasingly feasible.

JEL Classification: D82, H26, Q18

1. Introduction

Section 45Z of the Internal Revenue Code provides a clean fuel production credit for qualifying transportation fuel produced domestically after December 31, 2024, and sold by December 31, 2029. In February 2026, Treasury and the IRS issued proposed regulations addressing credit eligibility, emissions rates, certification, registration, reporting, and recordkeeping.

A significant policy question remains upstream of those administrative details: how should the government verify agricultural practices that affect the claimed carbon intensity of biofuel feedstocks when those practices occur on specific fields, in specific crop years, and are not directly observed by the party paying the credit?

This paper argues that the upstream verification problem in §45Z is best understood not merely as a documentation issue, but as an observability problem within the economics of moral hazard. The paper does not attempt to measure realized overstatement in §45Z claims. Nor does it argue that farmers, aggregators, certifiers, or fuel producers are acting in bad faith. Its claim is structural: where credit value depends on field-level facts that are privately known to the reporting side but costly for the government to observe independently, economic theory predicts incentives consistent with overstatement unless observability is strengthened.

The argument sits at the intersection of three related literatures: the economics of tax compliance visibility (Kleven et al., 2011; Boning et al., 2025), third-party reporting as a compliance mechanism (Kleven, Kreiner, and Saez, 2016), and measurement, reporting, and verification for environmental claims (ICVCM, 2024).

2. Moral hazard, information asymmetry, and observability

In economic usage, moral hazard refers to situations in which one party’s behavior changes because the consequences of that behavior are not fully borne by that party and because the relevant action is imperfectly observable to another. The concept is frequently misunderstood as a moral accusation. The classic literature treats it as a structural feature of institutional design.

Two conditions are central:

Information asymmetry. The farmer or field-level operator knows more about actual tillage, cover-crop establishment, nutrient application practices, and crop-history details than the government can know from the claim file alone.

Cost displacement. If a reported practice lowers modeled carbon intensity and increases credit value, but the government bears the fiscal risk of any overstatement, then the economic structure contains partial cost displacement.

Neither condition is sufficient to prove fraud. Together, however, they create an environment in which the reporting side may face incentives that are not fully aligned with the relying side’s interest in accuracy.

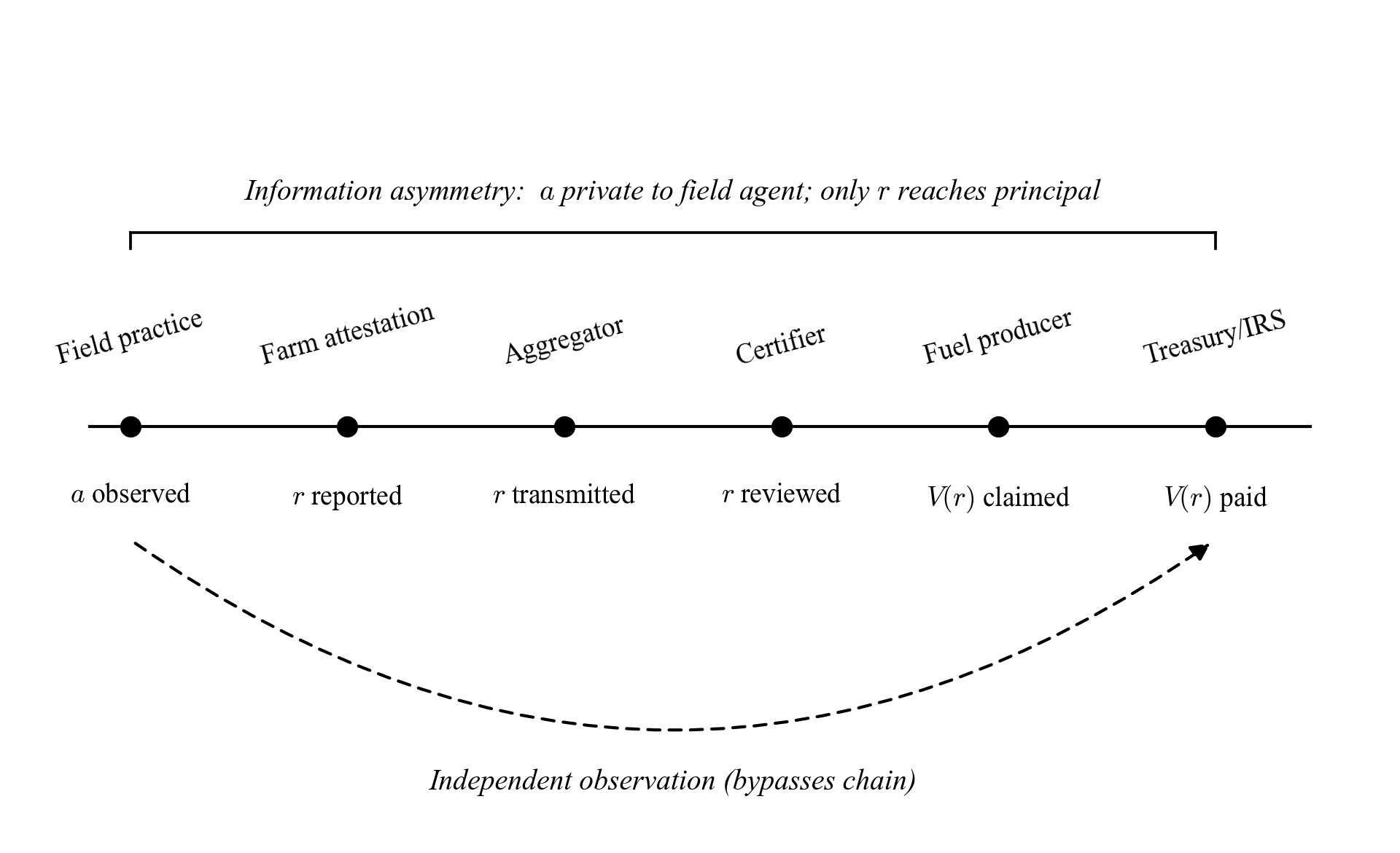

3. The §45Z verification chain as a principal-agent problem

The upstream verification problem can be represented as a layered principal-agent system. The principal is the government, acting on behalf of the public fisc. The field-level agent possesses private information about what actually occurred on a field in a given crop year. Between them sit intermediaries: first points of aggregation, intermediary entities, verifiers, and the fuel producer.

The information asymmetry originates at the field but propagates through the chain. By the time the claim reaches the principal, the underlying fact has been translated into records, attestations, and compliance artifacts that are useful but not identical to direct observation.

Figure 1. Information asymmetry in the §45Z verification chain. The actual practice is privately observed at the field level. Only the report propagates through the supply chain to the principal. Independent observation creates a direct evidence channel bypassing the reporting chain.

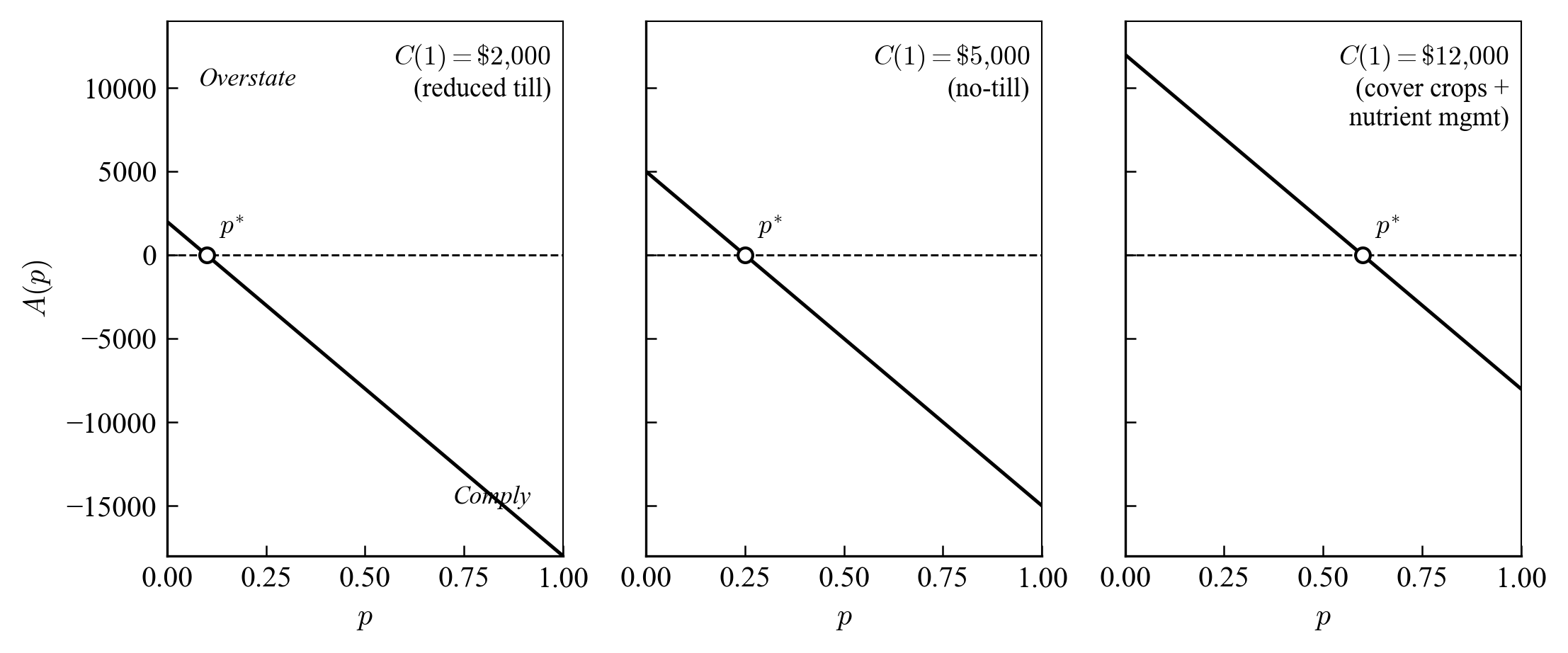

3.1 Formal representation

Let a denote whether a qualifying practice actually occurred, r the reported practice, V(r) the credit value, C(a) the private cost of performing the practice, p the detection probability, and F the expected consequence of detected inaccuracy:

E[Uₐ] = V(r) − C(a) − p · F · I(r > a)

The deviation advantage reduces to A(p) = C(1) − p·F, crossing zero at p* = C(1)/F. For detection probabilities below p*, overstatement becomes privately advantageous. Higher-cost practices require higher detection probability to deter overstatement.

Figure 2. Overstatement advantage for three practice cost levels. The zero-crossing p* = C(1)/F shifts right as C(1) increases. Practice cost values are illustrative comparative statics. F = $20,000 in all panels.

4. Welfare loss and regime comparison

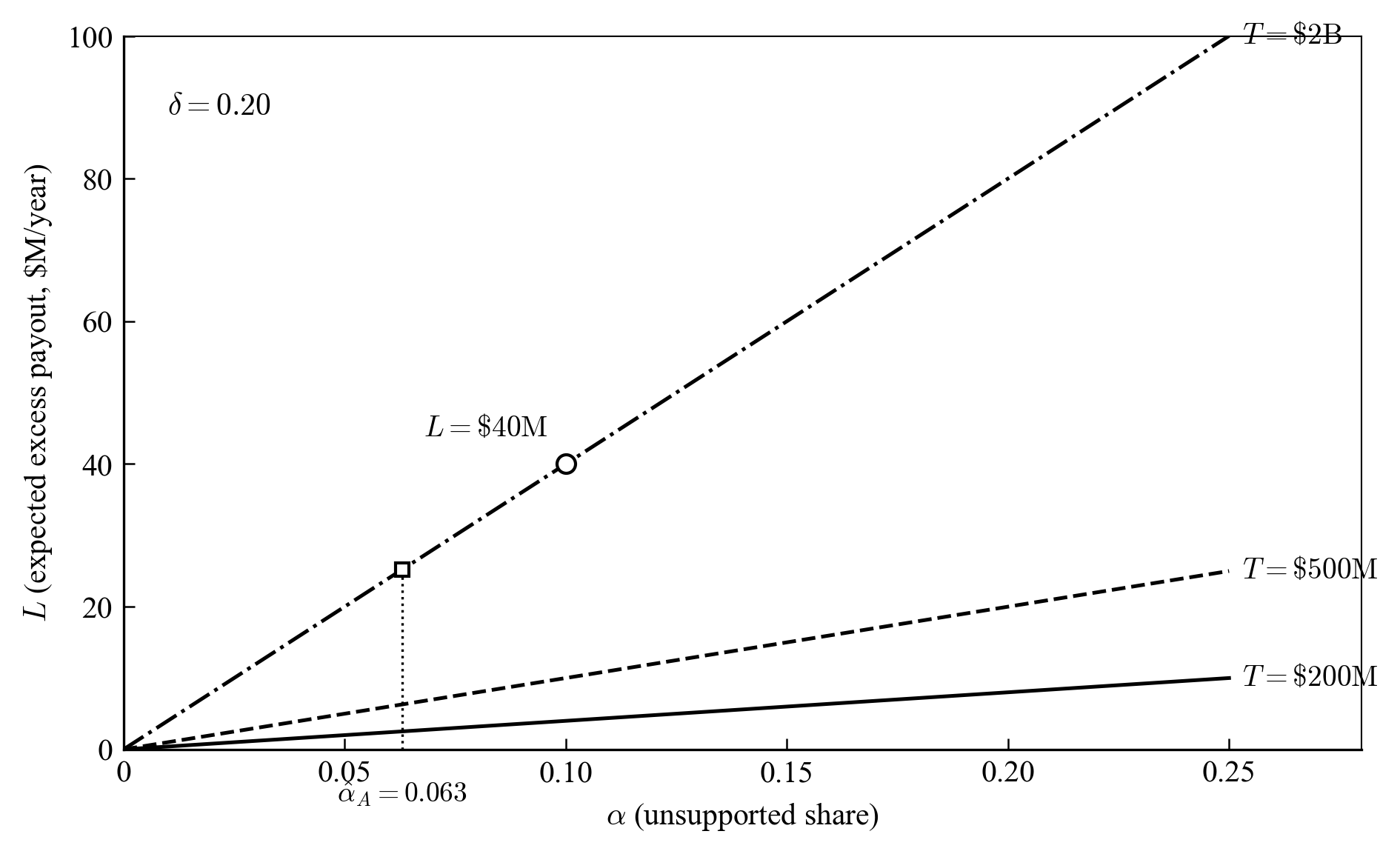

Tax administration provides an instructive analogy. Kleven et al. (2011) find that evasion is near zero for third-party-reported income but substantial for self-reported income. To formalize the aggregate consequence:

L = T · α · δ

Where T is total credit exposure, α is the share associated with unsupported representations, and δ is the marginal excess payout. Expected fiscal loss rises with exposure, with the unsupported share, and with the marginal value effect.

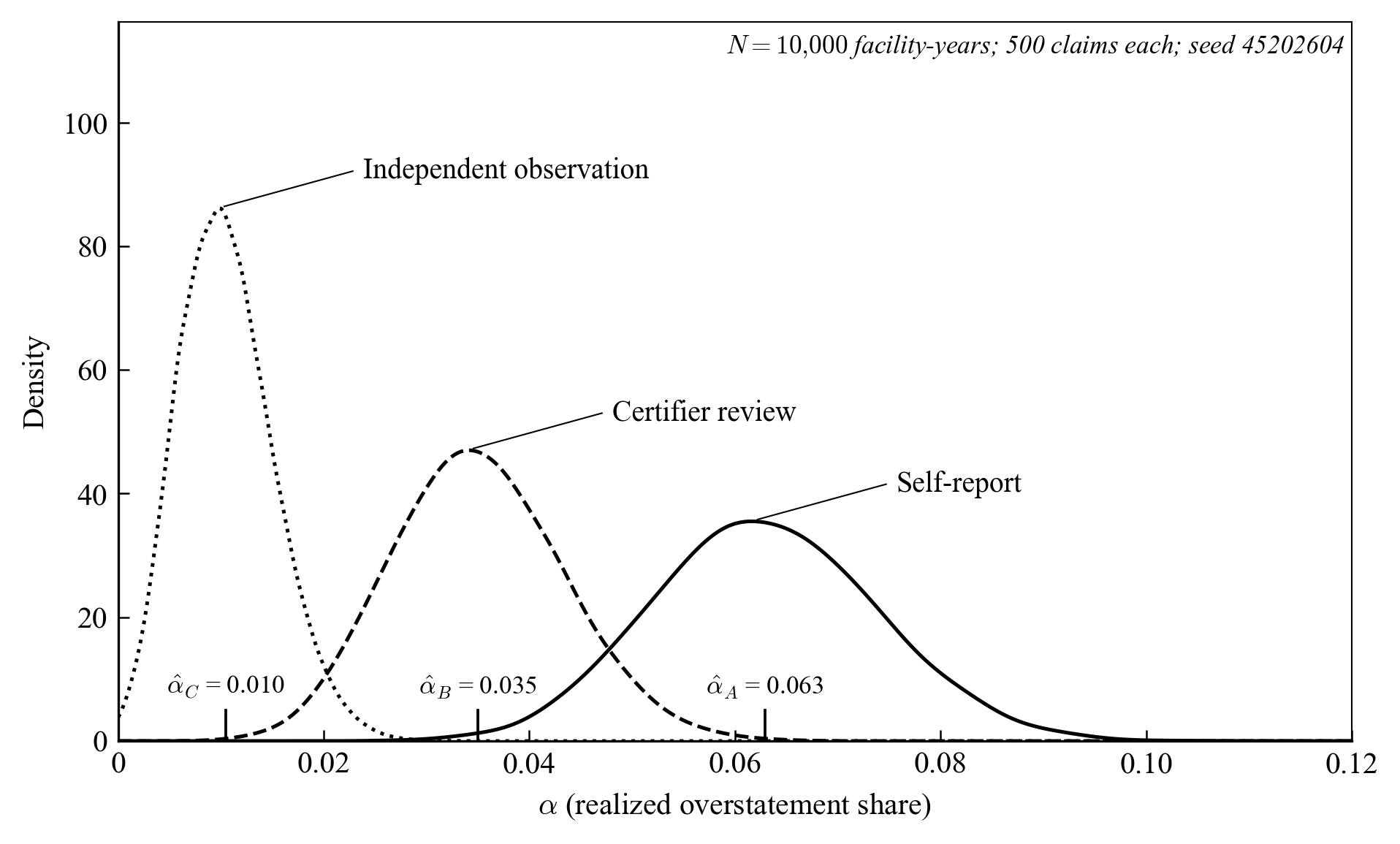

4.1 Monte Carlo simulation

To illustrate how α distributes under alternative regimes, we simulated 10,000 facility-years comprising 500 field-claims each. Actual practice adoption follows Bernoulli(0.65). Reporting accuracy varies by regime:

| Regime | Accuracy | Mean α | Implication |

|---|---|---|---|

| Self-report | 82% | 0.063 | ~$25M/yr excess at $2B exposure |

| Certifier review | 90% | 0.035 | Intermediate reduction |

| Independent observation | 97% | 0.011 | Both shifts and compresses distribution |

Independent observation both shifts and compresses the overstatement distribution. The central finding is stable across the parameter space examined.

Figure 3. Distribution of realized overstatement share under three verification regimes. Kernel density estimates from 10,000 simulated facility-years. Independent observation both shifts and compresses the distribution.

Figure 4. Expected excess payout as a function of unsupported share. Three lines represent total credit exposure levels. Vertical dotted line marks the Monte Carlo estimate α̂₀ = 0.063. δ = 0.20. Stylized representation.

5. Observation as the ex ante remedy

The classic literature offers two responses to moral-hazard risk: increase the agent’s downside exposure, or improve observation. The current §45Z framework emphasizes the first through certification, recordkeeping, and registration requirements. But ex post consequences are only as effective as the system’s detection capability.

Observation is the more efficient ex ante remedy because it changes the incentive calculus before the claim is made.

Independent observation shifts the effective detection probability p rightward, moving the agent from the region where overstatement is privately advantageous into the compliance region.

6. A governance analogy: 1040 evidence and 10-K stakes

A 1040 system tolerates substantial reliance on self-reporting backed by selective audit. A 10-K system operates under stronger controls because stakes, reliance interests, and materiality are higher — a principle codified in Sarbanes-Oxley Section 404.

| Governance pillar | 1040 posture (current §45Z) | 10-K posture (with observation) |

|---|---|---|

| Source documentation | Filer-assembled records | Independently generated observations |

| Internal controls | None at practice level | Structured methodology with uncertainty quantification |

| Consistency | Heterogeneous farmer narratives | Standardized across fields, counties, and crop years |

| Audit readiness | Reactive | Proactive — evidence precedes claim |

Where a tax-credit program generates large claims depending on upstream facts not directly observed by the payer, the evidentiary posture should move toward the 10-K side.

7. What this argument does not claim

This paper does not claim that current §45Z participants are acting fraudulently. A moral-hazard framework identifies structural conditions under which incentives may diverge from the principal’s interest in accuracy.

This paper does not claim that all upstream practice documentation is unreliable. Documentation controls and fact observability are distinct functions.

This paper does not claim that independent observation eliminates all dispute. What observation offers is a structurally stronger evidentiary posture than reliance on self-reported upstream facts alone.

The case for independent observation is strongest when framed as protection for honest participants, the Treasury, and the long-run credibility of the clean fuel program.

8. Policy implications

First, final §45Z implementation should recognize the distinction between documentation control and fact observability.

Second, independent field-level observation should be treated as a verification function, not an optional enhancement.

Third, the observation layer should be structurally independent of the claiming chain.

9. Conclusion

The upstream verification problem in §45Z is an observability problem in a high-value tax-credit system. When claim value depends on field-level practices privately known to the reporting side and only imperfectly visible to the paying side, the economic conditions that make moral-hazard risk salient are present. The appropriate response is not to presume misconduct, but to strengthen the structure of verification.

If final §45Z implementation aspires to 10-K-scale confidence, it will require more than 1040-style evidence. It will require an independent evidence layer capable of linking reported upstream practices to observable reality.

Selected references

Arrow, K. J. (1963). Uncertainty and the Welfare Economics of Medical Care. American Economic Review, 53(5), 941–973.

Boning, W. C., Hendren, N., Sprung-Keyser, B., & Stuart, E. (2025). A Welfare Analysis of Tax Audits Across the Income Distribution. Quarterly Journal of Economics, 140(1), 63–112.

Holmström, B. (1979). Moral Hazard and Observability. Bell Journal of Economics, 10(1), 74–91.

Kleven, H. J., Knudsen, M. B., Kreiner, C. T., Pedersen, S., & Saez, E. (2011). Unwilling or Unable to Cheat? Evidence from a Tax Audit Experiment in Denmark. Econometrica, 79(3), 651–692.

Kleven, H. J., Kreiner, C. T., & Saez, E. (2016). Why Can Modern Governments Tax So Much? An Agency Model of Firms as Fiscal Intermediaries. Economica, 83(330), 219–246.

Pauly, M. V. (1968). The Economics of Moral Hazard: Comment. American Economic Review, 58(3), 531–537.

Shavell, S. (1979). On Moral Hazard and Insurance. Quarterly Journal of Economics, 93(4), 541–562.

Download the full paper

Get the complete working paper with Monte Carlo simulation methodology, sensitivity analysis, and full reference list.

Register to download →